{kind=link}

The 401(okay) assertion has been sitting in your inbox for 3 weeks, unopened. You understand the drill: you click on it, see a steadiness that feels too small for somebody your age, get a small drop in your abdomen, and shut the tab. So you do not click on. You earn greater than you ever have, you may run a family finances in your head, and you continue to don’t have any clear reply to a easy query: are you really okay, money-wise? Years of that, and it has develop into the system: keep away from, really feel vaguely behind, repeat.

Determining how one can get your funds so as in your 40s has nothing to do with willpower you can not seem to discover. You run budgets at work. You handle a family. You aren’t financially illiterate. What’s lacking is a hard and fast order of operations on your cash, the identical type of sequence your job and your children’ schedule have already got. With out it, cash stays within the “I will take care of it” pile, subsequent to the opposite elements of life that preserve slipping when you deal with no matter is on hearth right now.

Proper now your cash runs on willpower. On this decade, with retirement lastly in view, it must run on a system as a substitute.

The place Ought to a 40-Yr-Previous Be Financially

A 40-year-old is “on monitor” with roughly thrice their annual wage saved for retirement (Constancy’s benchmark), three to 6 months of bills in an emergency fund, and high-interest debt beneath management. However most individuals aren’t there, and that’s regular, not a verdict. The median 40-year-old holds about $37,700 in monetary property outdoors dwelling fairness, and almost 40% of People of their 40s don’t have any retirement financial savings in any respect. [1]

So if you happen to really feel behind, you might have a variety of firm. The benchmark is a goal, not a scoreboard you’ve got already misplaced. And this is the half that issues greater than the quantity: your 40s are peak incomes years, and compound curiosity nonetheless has 20 to 25 years of runway earlier than retirement, which makes catch-up saving on this decade repay way over it can later. That runway can also be why it pays to start out treating retirement saving as one thing you may nonetheless make amends for slightly than a verdict that is already in.

The mathematics is blunt. Beginning at 40, saving about $15,000 a yr reaches a $1M goal by 65 at a 7% return. Wait till 50 and also you want almost $37,500 a yr to hit the identical quantity. [2] That is the entire cause monetary planning in your 40s feels pressing in a method it did not at 30. The price of ready simply acquired steep. The window continues to be vast open.

Why “Getting Organized” Retains Failing You

Getting your funds so as retains failing since you deal with cash as one big chaotic venture as a substitute of a brief sequence of small, ordered strikes. Confronted with a tangle of accounts, money owed, retirement selections, and faculty worries, the mind does what brains do beneath overwhelm: it picks the straightforward default, which is to shut the tab. The repair isn’t a marathon budgeting session. It is deciding the order as soon as, automating step one, and by no means having to summon willpower once more.

There’s analysis behind that avoidance. Underneath stress and overload, folks lean on inertia and the established order, which is precisely why most people by no means change a default as soon as it is set. Behavioral economists Benartzi and Thaler confirmed it is a two-way avenue: inertia retains folks caught, but it surely additionally turns into a robust instrument the second a very good default is in place, like computerized enrollment in a retirement plan. [3]

This is identical entice that reveals up in all places else in midlife. The routine you meant to maintain, the well being behavior you deserted, the cash test you postponed: all of it dies the identical method, postponed to a calmer week that by no means comes. We have written about that sample within the broader midlife reset, and cash is simply the area folks keep away from the longest as a result of the numbers really feel like a judgment. A part of the repair is loosening the cash mindset that treats each assertion as a report card, so opening the tab stops feeling like a verdict.

So cease attempting to “get organized” by effort. Effort is the factor that runs out. What survives a chaotic month is construction that runs with out you.

The Order of Operations That Really Works

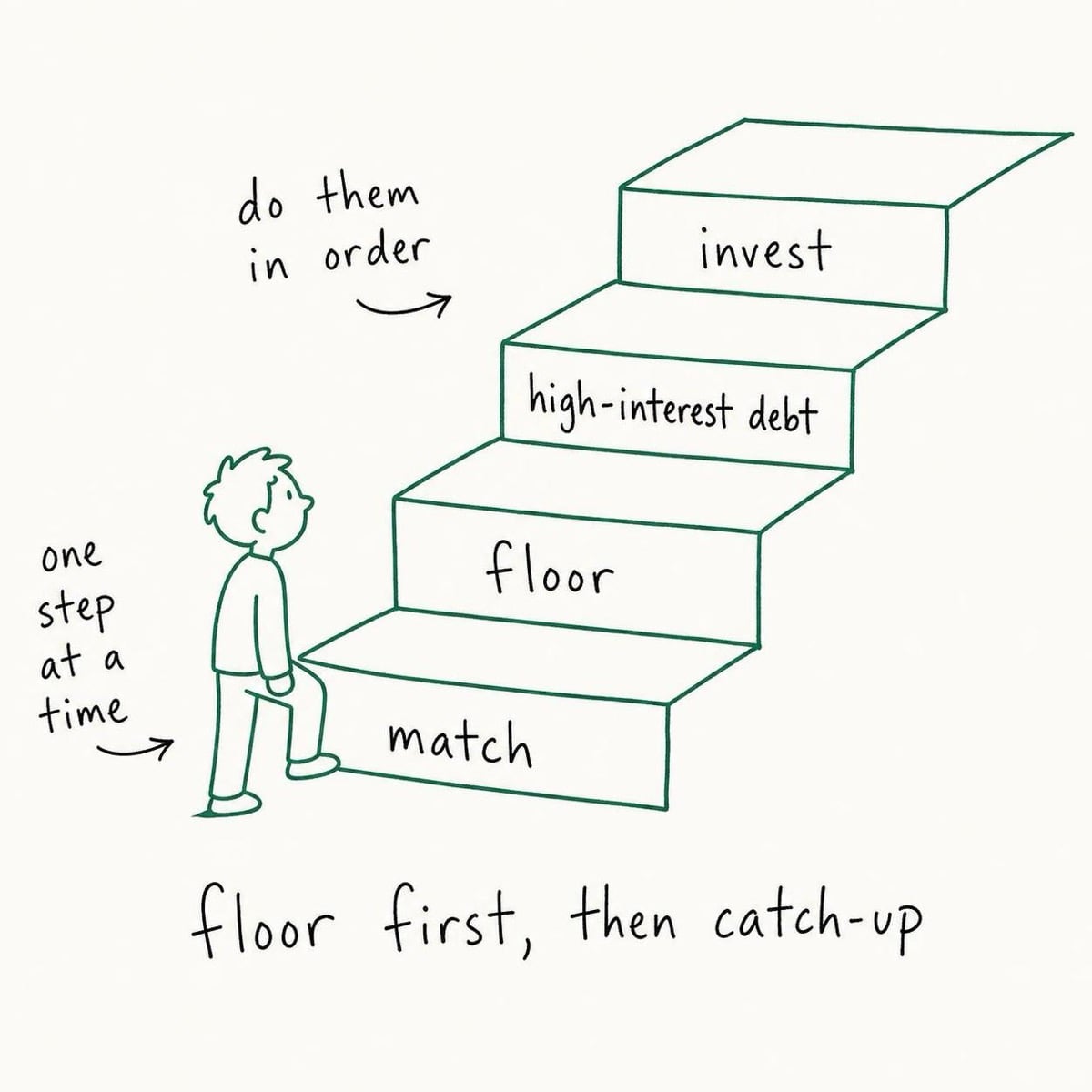

The reframe that fixes your funds in your 40s: there’s a appropriate order for each spare greenback, and following it beats budgeting more durable. You needn’t optimize every little thing without delay. You could know which greenback goes the place first. Vanguard’s framework ranks it cleanly: seize the complete employer 401(okay) match (the best assured return you will ever get), construct a starter emergency fund, kill high-interest debt, then put extra towards retirement. [4]

Stroll by it in plain phrases, as a result of the order is the entire level.

First, seize the match. In case your employer matches 401(okay) contributions and you are not contributing sufficient to get all of it, you might be turning down a 50% to 100% on the spot return. Nothing else on this listing beats that. [5] That is the only best-returning transfer in retirement planning in your 40s, and it takes one type and ten minutes.

Second, construct the ground. A small emergency fund is the ground methodology utilized to cash: just a few thousand {dollars} in a separate account, sufficient to soak up a shock with out reaching for a bank card. Set the minimal that allows you to breathe, then cease optimizing it. Vanguard discovered that holding simply $2,000 in emergency financial savings raised folks’s monetary well-being by 21%, with one other 13% acquire as soon as they reached three to 6 months of bills. [6] The calm you are after has a price ticket, and it is surprisingly small.

Third, kill high-interest debt. Something above roughly 20% APR (most bank cards) will get attacked subsequent, as a result of no funding reliably beats that fee. Paying off a 22% steadiness is a assured 22% return. [5]

Fourth, feed retirement. Now you push previous the match into the remainder of your retirement financial savings and longer-term investing. By your 40s you additionally get IRS catch-up room, the additional contribution limits that exist exactly for this decade.

This sequence is why we preserve saying: rebuild one system at a time, in the suitable order. Cash isn’t completely different from the remainder of the rebuild. It simply wants its personal queue. That’s the actual reply to how one can get your funds so as in your 40s: no more effort, a settled order. If the investing piece is the place you stall, the fundamentals of how one can make investments with out overthinking it clear a lot of the fog, and the day-to-day aspect is simply higher cash habits working on a schedule.

What This Appears to be like Like on a Actual Month

This is the order of operations as a lived month, not a concept. Marco is 47, an operations supervisor, married, two children, a automobile mortgage, a bank card steadiness he is been “which means to take care of,” and a 401(okay) he contributes 3% to with out figuring out his employer matches as much as 5%. He earns effectively. He nonetheless feels behind each time the subject comes up, which is why the subject not often comes up.

He would not finances more durable. He runs the sequence as soon as.

Saturday morning, espresso in hand, he does the 1st step: bumps his 401(okay) from 3% to five% to seize the complete match. Ten minutes, on-line, finished. That single transfer is free cash he was leaving on the desk each paycheck. Step two, he opens a separate high-yield financial savings account and units a $200 computerized switch for the day after payday, constructing towards a starter emergency fund. He would not have to recollect it or really feel motivated. The switch occurs whether or not or not it is a good week. That is your entire trick: automation beats willpower, the identical method an anchored cue beats a very good temper once you’re attempting to keep in keeping with any objective.

The bank card is subsequent within the queue, not right now. He lists the steadiness and the speed, factors his additional money at it after the match and the starter ground, and leaves the automobile mortgage alone as a result of its fee is low. He would not contact investing technique but. One queue, so as. No spreadsheet color-coding, no app with 40 classes, no Sunday-night dread. Three selections, two of them automated, and the fourth one parked till the third is completed.

That is additionally how the Save Extra Tomorrow program acquired abnormal employees from a 3.5% financial savings fee to 13.6% over 40 months: not by demanding self-discipline, however by tying financial savings will increase to future raises and letting inertia do the work. As soon as enrolled, 80% stayed in by 4 or extra pay raises. [7] Marco copies the thought: he units his 401(okay) to auto-escalate 1% yearly. He’ll be saving way more in 5 years and can barely really feel it.

A yr in, Marco is not a extra disciplined particular person. He is the identical particular person working a cash system that does not ask him to be disciplined.

The Fast-Math Guidelines, Decoded

These cash “guidelines” floating round (the $27.40 rule, the 3-6-9 rule, the $1,000-a-month rule) are psychological shortcuts, not legal guidelines. They’re helpful as tough targets to anchor a imprecise objective, and ineffective in the event that they exchange the order of operations above. The $27.40 rule says saving $27.40 a day equals $10,000 a yr, a technique to shrink a giant annual objective right into a every day one. The $1,000-a-month rule estimates you want about $240,000 saved for each $1,000 of month-to-month retirement earnings you need, at a 5% withdrawal fee.

The three-6-9 rule is the best for constructing the ground we simply coated: goal for 3 months of bills saved first, then 6, then 9 as your emergency cushion grows. It turns “save extra” into three concrete checkpoints. Deal with all of those as budgeting ideas on your 40s that make summary monetary objectives really feel reachable, not as a technique by themselves. The technique is the sequence. The principles are simply friendlier methods to dimension every step.

Cash administration in your 40s will get simpler once you cease chasing the proper rule and begin working a good-enough one on autopilot. A tough plan you really observe beats an ideal plan you keep away from. That is true for cash, and it is the identical fact behind any sturdy every day routine: the system you retain wins over the system you admire.

However You’ve got Tried to Repair Your Funds Earlier than

Honest. Most individuals have began a finances, tracked spending for 2 weeks, and give up. The same old cause is not weak spot. It is that you simply tried to repair every little thing without delay by guide effort, which is identical overwhelm in a spreadsheet. The order of operations works in another way: you make a handful of one-time selections, automate them, and cease counting on month-to-month motivation that was at all times going to fade.

The opposite objection is time, and cash rewards the impatient right here. You do not want a weekend. You want the following half-hour to do precisely one factor: seize your employer match. That is the highest-return transfer on your entire listing, and it is a single type. Every little thing else can await subsequent Saturday.

And the “my state of affairs is extra sophisticated” objection normally is not, no less than not for the primary three steps. A messier steadiness sheet (a aspect enterprise, a second mortgage, an outdated 401(okay) from a job two employers in the past) adjustments the later optimization, not the order you begin in. Match, ground, high-interest debt: that sequence holds whether or not your funds are easy or tangled. The complexity lives downstream, after the fundamentals are working. This identical “shrink it, automate it, sequence it” logic is what makes a monetary guidelines on your 40s one thing you end as a substitute of one thing you flinch at, and it plugs straight into making a life plan that treats cash as one area amongst work, well being, and household slightly than a separate disaster.

Begin With One Transfer This Week

Open your retirement account right now and test one quantity: are you contributing sufficient to get your full employer match? If not, elevate it till you might be. That is the only highest-return monetary determination out there to you, and it takes about ten minutes. Then decide the following merchandise within the queue (a small computerized switch to a starter emergency fund) and schedule it for the day after your subsequent paycheck.

That is how one can get your funds so as in your 40s with out a budgeting overhaul or a character change. Not 20 hacks. One ordered sequence, automated step-by-step, working quietly beneath a busy life. Cash turns into one calm system as a substitute of the factor you retain avoiding, and it sits subsequent to the remainder of your rebuild as a substitute of separate from it. Seize the match this week, and each quiet paycheck after that does the compounding you’ve got been pushing aside.

Continuously Requested Questions

The place ought to a 40 yr outdated be financially?

A standard benchmark is roughly thrice your annual wage saved for retirement by 40 (Constancy’s guideline), three to 6 months of bills in an emergency fund, and high-interest debt beneath management. Most individuals fall in need of this. The median 40-year-old holds about $37,700 in monetary property outdoors their dwelling, so deal with the benchmark as a goal to goal at, not a scoreboard you’ve got already misplaced.

What’s the $27.40 rule?

The $27.40 rule is a financial savings shortcut: $27.40 a day provides as much as about $10,000 in a yr. It sizes a financial savings goal, but it surely doesn’t determine the place that cash goes first. The article walks by the way it suits the order of operations.

What’s the 3 6 9 rule in finance?

The three-6-9 rule is a staged emergency-fund goal: three months of bills saved first, then six, then 9. It is a technique to construct the ground in concrete checkpoints. The article covers the place it sits within the full sequence.

What’s the $1000 a month rule?

The $1,000-a-month rule estimates you want about $240,000 saved for each $1,000 of month-to-month retirement earnings, at a 5% withdrawal fee. It is a sizing shortcut, not a technique. The article explains the sequence that truly will get you there.